Money causes most marital fights they say.

I completely agree.

Have you ever had a disagreement over money? (see my questions and comment below!)

Too much of it, too little of it, how it’s spent, how it’s saved….even how it is organized can cause contention.

Once my husband and I had a spat over which category the new lawn mower should be put under. The home and food budget? Family Purchases? Miscellaneous? I look back and think, like, really??? and did we really have that many categories to choose from?

So this summer has been pretty epic in the procrastination department. On my part with my blogging goals that is. We have been playing it up in the sun and the water, trying to escape the Texas meltdown. I am super late getting my thoughts down here on the blog. June was all about budgeting and here we are at the end of July! And July is about saying no- or the art of essentialism…how ironic considering i have been saying yes to all the fun things such as lake days and movie nights with hubby! haha. But here I am and I promise to myself, and to you, that all the thoughts and studies and ideas will be up here shortly.

So what does money fights and summer procrastination and all that have anything to do with each other? Look at this picture of husband and I just recently at a pool party:

See the genuine happy there? Now I’m not sayin it is all bliss and glory. Oh no. It is hard work all right. But there is a heck of a lot more of that happy since we ditched switched to a reverse budget method earlier this year after, ahem, almost 11 years of excel line item traditional budgeting. Is that what is making this summer easier and more happy? I’d like to think it is playing a big part.

I read a couple of books…does this come as any surprise? I think my blog title should be something to do with book reports – I feel like every post is a review on books I’ve read! haha! I’m on a serious learning curve this year.

Well, a couple of years ago my husband had me read Automatic Millionaire by David Bach. I have now probably recommended and/or given it away to like 30 people, no joke. It is an awesome read. Short, to the point, and memorable -it will have you thinking deeply about what you can do to start becoming a millionaire – TODAY. Keep a lookout on my Instagram @imsimply_taylor cuz I plan to do a budget topic giveaway soon and whataya know, a copy of Automatic Millionaire is sure to be a part of it!!!

Prior to starting this blog and when I initially began my simplicity journey I read Living Well Spending Less by Ruth Soukup. I mentioned this book a while back in my Rise and Shine post and have it listed in my recommended reads. This book is a great platform for looking at the way you run your life and your house. She is super down to earth and tells her story like it is- totally raw, the good and the bad. Shopaholic turned coupon-er with a marriage that suffered and then flourished as the money situation got under control.

Both books provide great ways to get your financial life in order.

I am going to first state that before reading on- if you are severely in debt- a system like Dave Ramsey’s might be best for you before you start anything else. I have heard good things about it. Once again the clear the chaos/clutter before anything else will stick idea is at play here. Just like with our kids and discipline . Pay down your debts first.

Luckily we have always been of the mindset, both my husband(yes) and I(ideally), that we should live beneath our means as much as possible and not incur credit card debt. In fact we didn’t really have credit cards until not that many years ago! Which honestly wasn’t great either because we are

new to credit history and that isn’t helpful sometimes. However, it did help us all through college, dental school and residency to keep our debts to a bare minimum- really only school and a small car payment at the end of residency. We even managed to get through 4 years of dental school with 1 cash purchased vehicle between the two of us -there was a lot of walking in the dead of a Cleveland winter!

That being said there was still a great weight and a burden every month. Let’s be honest I was never great at getting it all recorded and sometimes it was like every other month- or longer! Yikes. As budget review came around I felt guilty that things didn’t look better, and Matt, I mean, husband, felt upset that we weren’t in better standing and I was late getting it done. I sincerely hated itemizing every single penny, transferring bank account statements and receipts to lines in excel, and haggling over where every unplanned expense should go; he hated it not being done on time so he could have a good look at our financial standing and we struggled over reviewing it every. single. time. It caused contention and while I can say it was probably mostly my fault, I knew we had to find a method that worked for both of us.

Once we entered paycheck status a few years ago it was brutally clear we needed a better way. Expenses bloomed where there had been none before, old things from 10 years of marriage needed replacing, and we didn’t have to live like starving students anymore. Now there were more lines in the budget, like student loan payments and kids expenses and the possibility of vacation. It made my head spin just opening that blasted excel spreadsheet and transferring all that data from mint into each line and double checking every expense. I sound like a dramatic diva but I really truly hate it. I have other strengths in life, and I have never put us in debt. I can now admit that this is not one of my strengths and that is ok. I could find a way to make “budgeting” work for me and be good at it. I just needed to find the way.

So how do we do it? Why are things less stressful, simpler, and more joyful around here?

Because of the “pay yourself first” method. Or Reverse Budgeting.

Anything that sounds like not budgeting or the opposite of budgeting sounds interesting to me. hehehehe

Get Automatic Millionaire or just google it and you’ll get more details.

Here is the gist of it: PAY YOURSELF FIRST. And do it AUTOMATICALLY.

Step 1: Sit down and figure out your fixed and variable expenses. If you aren’t an avid budgeter as of now you may be wondering what those are. Boiled down it’s the stuff you pay over and over and the stuff that changes every month. Think bills and utilities versus food and clothes.

Step 2: Automate your bill payments on fixed expenses and ALSO on savings. Make sure you are paying your bills and yourself every month. Even if it is only $10. Get it out of your paycheck and to the utility company and your separate savings (read:untouchable without effort) account. By the time we even get around to checking our account each month the car payment and phone bill (among other bills) have been made and fixed amounts have been transferred to our online savings and house down payment accounts with Capital One. We have now met our emergency account goal but that was once fed too.

Step 3: Take a look at what is left of your money after fixed costs and savings. This amount is for EVERYTHING ELSE. All the variable expenses like food and fun + credit cards! If what you spend each month can’t be paid off with what is left in your account then it is time to cut costs.

Step/Thought 4: The extras will kill you. The latte (wait I don’t drink coffee…sooo the smoothie maybe?) the nails, the eating out, the cute water bottle, the toys in the checkout line- those are the little things that will eat your savings potential right up. I’ve been there. I know. Amazon and I have an understanding now. We have determined our relationship. I will stay signed up, and she will not send me little eggs filled with surprises for my children to open on our road-trip in two days because I saw it on Pinterest. Oh. There is another DTR I will have to have soon.

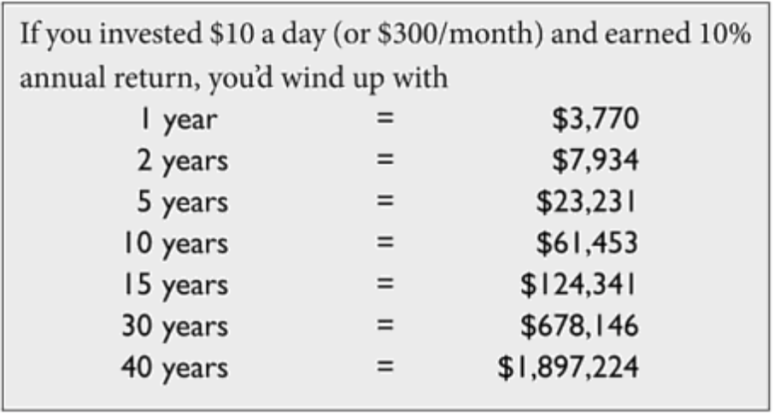

I don’t live on a spreadsheet anymore. Neither should you if it is making you crazy. Try doing your budget in reverse. Pay yourself first. Spend a little less, save a little more. Did you know that if you saved just one drink a day- let’s say your coffee or your sports drink or your soda- you could save like $250,000 in your lifetime? True. Here is a chart from the book if you don’t believe me:

This might be worth exploring huh? This return might be a bit high in todays market…but even at a fraction of that you can seen how paying yourself first and saving is really a good-looking idea!

So go for it! Try paying yourself first. Simplify your budget and the way you approach saving and spending. Once again, simplifying for the win.

Happy Summer

In case you missed the link above here is the first result from googling reverse budget:

Forbes: Creating a Budget that Actually Works

How do you handle your household expenses? Do you budget? How? Are you saving money? I would love to hear your ideas and what works- or doesn’t!